The first keynote address of this year’s Prospectors and Developers Association (PDAC) of Canada convention was particularly germane given that PDAC is the world’s largest mining conference, most publicly listed mineral companies are Canadian, and the majority of these have gold mining operations.

The talk, entitled The fate of gold deposits, was delivered by Douglas Silver, CEO of Flydentity LLC. He explored global gold endowment over the past 30 years.

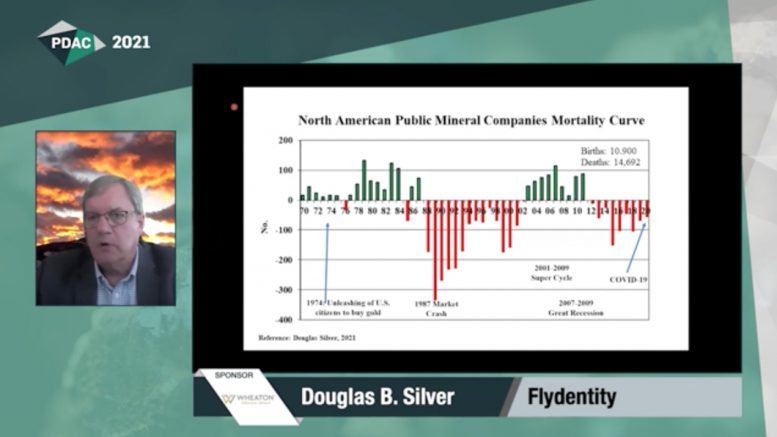

Silver said the idea for the talk started when he asked the question “What happened to the gold deposits of 1989?” during a keynote speech in 2019 at the 30th anniversary of the Denver Gold Group, which he founded in 1989.

He first started by developing a database containing 2,748 gold deposits dating back to 1989.

“I then systematically went through over 5,500 company websites on the Goldsheets mining directory to update old deposits and add new deposits,” he explained. “Missing data was fleshed out using The Northern Miner and the Mines Handbook, with specific data from Stockwatch, and I backfilled with data extracted from hundreds of NI 43-101 reports and company press releases,” he said.

Silver noted that many gold deposits disappear because they are either mined out, abandoned, or returned to their private owner. Deposits also change names, and operators often don’t disclose the termination of operations or dropped properties.

“In addition, the multiple expansions of large porphyry copper mines means that many [operators] no longer consider their precious metals as material and so don’t report them,” he said.

Older deposits, he added, are often incorporated into more significant deposits due to land consolidation and the push for larger mines, citing as examples the Canadian Malartic mine, jointly owned by Yamana Gold (TSX: YRI; NYSE: AUY) and Agnico Eagle Mines (TSX: AEM; NYSE: AEM), and the Super Pit in Western Australia operated by Kalgoorlie Consolidated Gold Mines, a joint venture between Barrick (TSX: ABX; NYSE: GOLD) and Newmont (TSX: NGT; NYSE: NEM).

In 1989, approximately 2.5 billion oz. of gold resources were held in 2,748 deposits, which, by 2020, had increased to 2.6 billion ounces. Although the number of million-plus-oz. deposits had declined from 414 in 1989 to 355 in 2020, the total gold resources for these deposits increased from 2.1 billion oz. to 2.5 billion oz. over the same period, Silver said.

While the proportion of million-plus-oz. deposits compared to total deposits declined from 15% to 13%, he noted that the share of gold production from these deposits compared with total production increased from 83% to 96% over the past 30 years.

Of the 2,748 deposits in 1989, 27.3% (750) went into production and 25.8% (710) are still known to host resources, he added. (When using “resources,” Silver notes that he is referring to a combination of measured, indicated, and inferred resources.)

“In 1989, most of the deposits were in Canada and the U.S.,” he said. “If you add in Mexico [in fifth place], then North America comprised 58% of the total deposits globally but only about 21% of the total gold production that year.”

South Africa, he continued, was the fourth-highest country (after Australia) for the number of deposits in 1989, producing over 600 million oz. of gold, the highest amount of any country that year. (Canada placed second at nearly 300 million ounces.) However, South Africa’s gold production has dropped to about 300 million oz. and is the world’s fourth-largest producer today, with Canada the number one producer at approximately 600 million ounces.

Outside the top 11 gold producing countries globally, the rest of the world accounted for over 600 million oz. of gold production in 1989 and over 1.6 billion oz. in 2020, with Ethiopia increasing its number of deposits by 400%, Finland by 400%, Saudi Arabia by 367%, Romania by 233%, and Armenia by 200% over this period, Silver explained.

“The database showed that 23 deposits representing a total of 147 million ounces of gold have been known about for 30-plus years but have never been placed in production,” he said. “Fifteen of these deposits are located in Canada, with six in the U.S., one in Peru, and one in Chile.”

According to Silver’s analysis, today’s gold deposits are larger in tonnage, have lower grades, and contain more ounces compared with deposits in 1989, which, he said, is primarily due to the higher gold prices and lower operating costs today.

He estimated that the average grade of deposits in 1989 was 1.37 grams gold per tonne, with those same deposits now showing 0.56 gram per tonne. Total tonnage for these deposits increased to 133.1 billion tonnes containing 4.1 billion ounces from 54.6 billion tonnes containing 2.4 billion oz. of gold over the past 30 years.

When new discoveries were included in the calculation, taking the total number of deposits to 3,721, the total tonnage was estimated to be 244.6 billion tonnes grading 0.52 gram gold containing 4.1 billion ounces.

“What you see here is classic resource management,” Silver explained. “By the end of 1989, the gold price was about US$409 per ounce, and by the close of December last year it was US$1,860 per ounce. So, when gold prices are low, you mine high grades, and when gold prices are high, like today, you mine low grades.”

The mix of mining methods has also changed over the past 30 years, with the proportion of open-pit mines increasing by 20% and the share of million-plus-oz. deposits that are open-pit mined jumping 35%, he noted, despite the impacts of open-pit mining on the environment.

Silver acknowledged that, although his database shows that there is about 4.4 billion oz. of gold resources today, this figure does not include gold from companies that are mining platinum group elements, which, could account for another million ounces, or gold mined at porphyry copper deposits, which can typically contain anywhere from a million to 10 million ounces.

“When you roll all this together, it amounts to probable resources of about 5.0 billion ounces, which, if mined at 100 million ounces per year provides for a 50-year supply,” he said. “Improvements in technology, which lead to lower operating costs and lower cut-off grades, combined with increases in gold prices could see a lot more gold being extracted.”

Be the first to comment on "PDAC: Exploring 30 years of global gold endowment with Flydentity’s Douglas Silver"