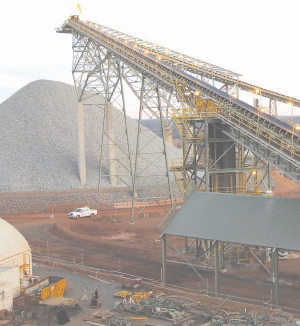

Newmont Mining’s (NMC-T, NEM-N) Boddington mine has, at last, swung into production.

The mine — which will be the largest gold mine in Australia once it ramps up to full production in 12 months’ time — represents the realization of a global strategy that has targeted Australia and the Asia Pacific area as it’s key growth region.

Such a desire was underlined at the end of June, when Newmont showed it was no longer content to have a partner at Boddington and acquired AngloGold Ashanti’s (AU-N, AGG-A) 33.33% interest in the project.

Sitting 130 km southeast of Perth, Newmont is expecting to get roughly 1 million oz. per year out of Boddington at a cost of just US$300 per oz. for the first five years of operation. The project has a mine life of roughly 24 years.

All of those ounces will be coming from a massive deposit that hosts proven and probable reserves of 793.6 million tonnes grading 0.79 gram gold and 0.11% cop- per for 20.1 million oz. gold and 873,000 tonnes copper.

And while those are eye-catching numbers, Newmont believes it will continue to add to them. If its recent drilling is any indication, the company stands a fair chance of doing so, considering that in 2007, reserves stood at 16.6 million oz. gold.

But a mine of Boddington’s size, in a politically stable, mining-friendly country doesn’t come cheaply.

Newmont had to pay AngloGold US$750 million in cash at the closing of the deal, plus another $240 million that could be paid in either cash or Newmont common stock, at Newmont’s option, in December. AngloGold also got a royalty capped at US$100 million.

And then there’s the cost of building the mine. Newmont estimates that when all is said and done, capital costs will be between US$2.6 billion and US$2.9 billion.

Such high costs were behind the project’s initial delays in 2008. The company pushed production back into mid-2009 because of inflationary cost pressure.

More recently, delays came from difficulties in getting the wet plant into commissioning. Newmont blamed the set back on wet weather and a decline in contracted workforce productivity.

Such delays didn’t come without costs to the company’s bottom line.

The later startup date at Boddington forced Newmont to lower its gold sales forecast for operations in Australia and New Zealand to between 1.4 and 1.5 million oz. It had previously given guidance of 1.5 to 1.6 million oz. for the region.

The delays also had a negative impact on overall costs. Newmont now says costs for 2009 will be between US$460 and US$500 per oz., higher than the previously announced guidance of US$440 to US$480 per oz.

With both the size of the Boddington project and its delays grabbing so much attention, what Newmont has already done in the region could easily be overlooked.

When the company’s mine in Indonesia and another in New Zealand are taken into account, the Asia Pacific region as a whole has grown to become Newmont’s largest asset.

In Australia, the company’s mines have benefitted recently from a combination of lower diesel costs and a weaker Australian dollar.

For the second quarter alone, Newmont produced 283,000 oz. gold from its Australian and New Zealand operations with average cash costs of US$500 per oz.

One of its most productive mines is Jundee. Currently, the mine is only an underground operation, but Newmont says there is open-pit potential looking out a year into the future.

For the first half of 2009, the mine managed to produce 202,000 oz. gold at a cost of US$345 per oz., down from US$410 the year before.

Newmont also has the Tanami mine in the country, which produced 173,000 oz. gold for the first half of the year at cash costs of US$586 per oz.

Production at Tanami, however, was lower this year than last due to lower mill ore grade. For the first half of 2008, the mine produced 190,000 oz. gold.

Over at Kalgoorlie — Australia’s second-largest mine — attributable production came in at 146,000 oz., up from 132,000 oz. produced over the same period last year.

Kalgoorlie is a 50/50 joint venture with Barrick Gold (ABX-T, ABX-N) and in January, the two companies won an environmental approval that will allow them to expand the site.

The trend towards lower costs carried over to Kalgoorlie as well, where costs fell to US$625 from US$817 an oz. a year earlier. Lower costs were coupled with a 13% increase in gold sales thanks to higher mill ore grade, throughput and recovery.

In New Zealand, the results weren’t quite so robust. An electrical fire at Newmont’s Waihi mine had the mill out of operation for more than two months. The shutdown cost the company roughly $50 million in lost revenue and caused production to slip to 56,000 oz. from 65,000 oz. in the first half of the year. In early August, however, the company had the mill back up and running.

Despite the continued strength in the price of gold, and resurgence in gold mining stocks that began in late March, Newmont hasn’t been able to translate its large gold operations into market success.

Since the beginning of the year, Newmont shares have traded relatively flat, beginning 2009 at US$41.39 and trading for US$41.40 at presstime.

Newmont must hope that all the ounces it is getting ready to pour from Boddington will help carry its share price to more market heights.

Be the first to comment on "Newmont Finds Pot Of Gold In Oz"