The amount spent to find new mineral sources may grow little next year, even if gold prices continue their record run and President-elect Donald Trump cuts red tape, according to S&P Global mining analysts.

Further easing of interest rates won’t significantly dent a tight financing market that will likely limit next year’s exploration budget increases. And that could raise concerns for majors who increasingly depend on their smaller counterparts for discoveries, analysts said during a webcast on Wednesday.

“The reality is that juniors often lead the charge in finding new deposits,” Mark Ferguson, director of metals and mining research, said during S&P Global’s quarterly State of the Market webinar. “When they’re underfunded, the whole pipeline feels it.”

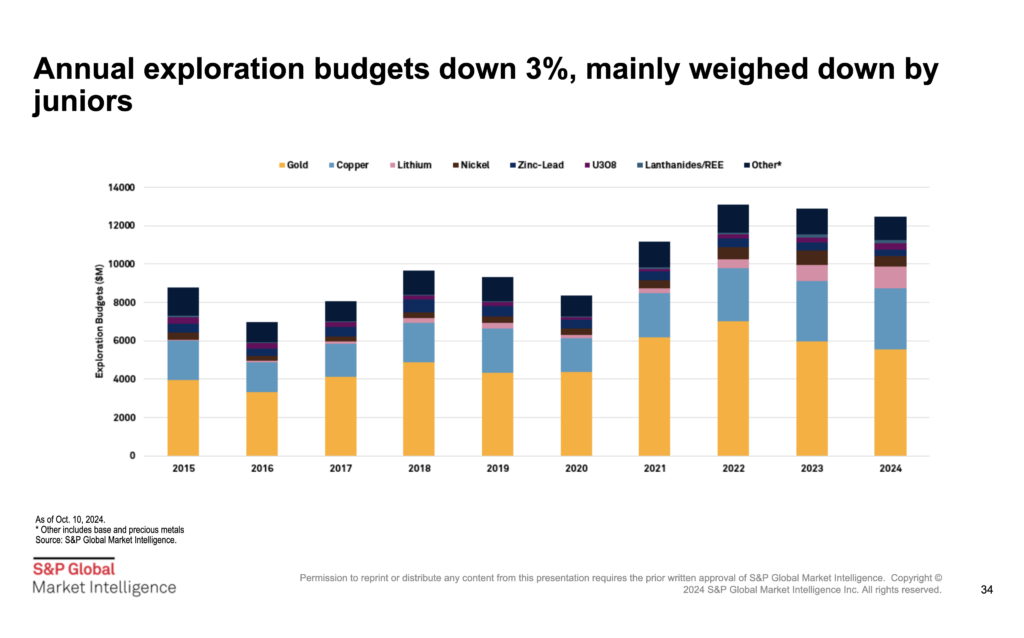

The cautious outlook comes as global exploration budgets for nonferrous metals declined by 3% in 2024 to US$12.5 billion from US$12.9 billion last year, with juniors bearing the brunt of the cuts. Some high commodity prices haven’t helped juniors raise capital. Even gold exploration is hurting.

Projects pipeline

The effects of shrinking budgets and financing struggles have shown up in S&P’s measure of new exploration activity. Its pipeline activity index (PAI), which tracks drilling, financing, and project milestones, dropped to 63 in the third quarter of 2024—the lowest level since 2016.

As new activity declined, the exploration price index (EPI) rose to a record high at 203. It reflects metals price trends that companies explore for, such as gold, copper, nickel, and others, and not the actual cost of exploration. The rise was due to steadily rising gold prices and a recovery in some other commodity prices.

The gap between the PAI and EPI shows that, while prices to sell some metals are good, investment in new projects is low. This signals that companies are prioritizing existing assets over high-risk exploration, S&P said.

“This trend (of lower exploration spending) aligned with a cautious investment landscape and a conservative approach from investors,” associate research analyst Jasper Madlangbayan said. “Juniors have faced some of the hardest hits as financing has dried up.”

Critical minerals

However, there could be resilience in critical minerals as economies shift to renewable energy and electrification, the analysts said.

“Critical minerals remain a bright spot,” Francesca Price, senior analyst for critical minerals at S&P Global, told the webinar. “There’s still investor interest in supply chains that secure access to these resources outside traditional, more geopolitically challenging regions.”

So far this year, overall drilling rates fell for nearly all metals. Nickel projects had 53% fewer drill holes than the previous quarter.

“Though we’ve seen significant decreases in drilling and new projects, there’s still hope for a recovery if metal prices hold steady,” Madlangbayan said.

For next year, the analysts expect copper prices to average US$9,825 per tonne on the London Metals Exchange compared with US$9,331.50 per tonne on Wednesday, driven by stock depletion and seasonal demand. Nickel is forecast to average US$16,995 per tonne versus US$15,897 per tonne now. They expect a surplus to be maintained by high output from Indonesia and China, which together will account for 78.2% of global production by 2028.

Geographic contrasts

Australia, home to many junior explorers, saw the largest budget drop as juniors struggled to finance projects. Western Australia, a hub for gold and base metals, suffered the most, S&P said.

“Australia’s large junior population is simply not able to support the same level of exploration that we’ve seen in previous years,” Madlangbayan noted.

By contrast, U.S. exploration spending rose, driven by increased copper and lithium allocations. Laws like the Inflation Reduction Act boosted domestic supplies of critical minerals by helping fund exploration budgets.

“The U.S. has shown resilience in exploration budgets, particularly in states like Nevada and Arizona, which have seen renewed interest due to policy incentives and their proximity to infrastructure,” Francesca Price, senior analyst for critical mineral research, said. “Sustained interest in the critical minerals supply chain should help buffer the sector from further declines in exploration.”

The metals and mining industry is split, Ferguson said. Major companies are expanding through acquisitions. Juniors are struggling for funds. This raises questions about the long-term health of new project development.

“The sector’s resilience is being tested,” Ferguson said. “But, with demand for critical minerals high, there’s hope. Exploration budgets may stabilize in 2025 for the key commodities of the energy transition.”

Be the first to comment on "Exploration spending to stay flat despite Trump pledges, strong gold prices, S&P says"